Tectonic Shift: Exploration Moves Offshore

“It’s a structural change”…”the most prolific reservoirs other than the Middle East are offshore. Period full stop. That oil in place, barrels in place, it’s just fundamentally better than other areas of investment for our clients.”

Doug Pferdehirt, CEO, TechnipFMC

A tectonic shift in the oil and gas industry is underway as explorers increasingly focus on offshore fields. This structural change in the industry is occurring as a bid to book reserves and plan for the future. U.S. shale oil which has driven global production growth over the past decade is entering a new era of higher costs and more complex development as shale plays mature and production growth slows. The industry is voting with its feet with capital increasingly being transferred from U.S. onshore to offshore according to Doug Pferdehirt, CEO of TechnipFMC¹. He also predicts that operators will increasingly treat their onshore assets as short cycle opportunities while moving toward offshore development to improve their reserve replacement ratios.

The breakeven price of shale wells in the United States currently sits at $70 per barrel but is expected to rise to $95 per barrel by 2035 according to Enervus. Shale drilling expanded rapidly because entry costs were lower and returns were faster than those of offshore drilling. But with the most prolific shale areas depleting in giant fields such as the Permian, shale producers need to shift drilling to less productive areas incurring higher costs.

The breakeven cost for U.S. shale oil is currently $70/bbl and Rystad Energy expects that to increase to $95/bbl by 2035.

The rapid growth of shale oil directly impacted offshore investment, particularly deepwater drilling. Total upstream offshore investments fell from $340 billion in 2014 to $140 billion in 2021 after which they began to rise, according to Rystad Energy. The oil price crash of 2014 has also served to reset exploration with budgets on a very tight leash. Fewer companies are active in exploration nowadays with it being primarily an exclusive group of super majors and national oil companies (NOCs).

This contrasts with offshore breakeven costs of $35-$45 per barrel.

Today offshore breakeven costs are in the $35-$45 per barrel range with offshore drilling accounting for ~30% of global oil production. Offshore exploration offers the potential for giant discoveries such as those in offshore Brazil, Namibia and Guyana while leaps in technology such as subsea engineering, robotics and floating production vessels has significantly lowered breakeven costs.

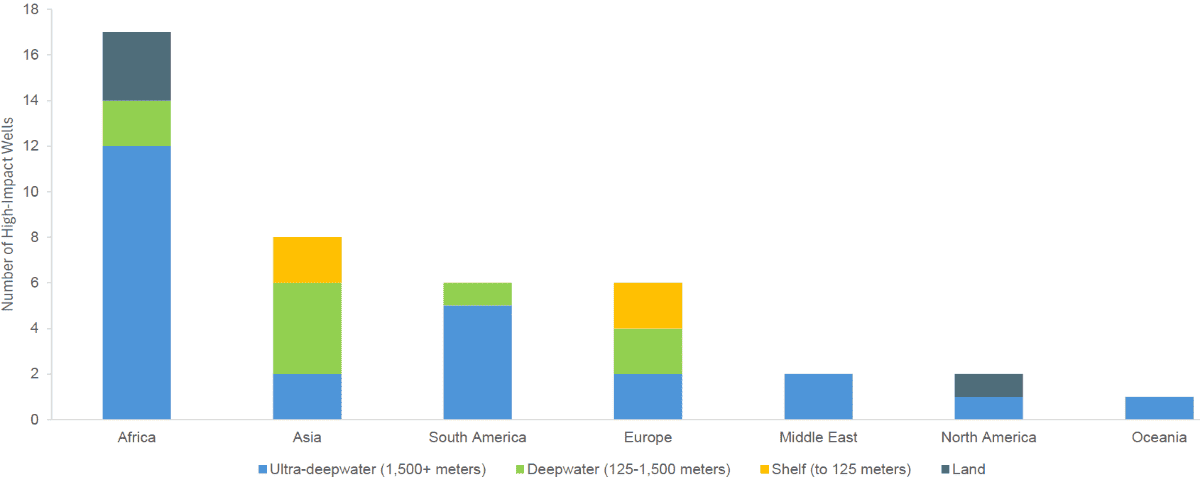

Global Majors Face a 300-Billion-Barrel Supply Shortfall by 2050

The 30 largest global oil companies face a 300- billion-barrel supply shortfall by 2050 an amount equivalent to 14 Guyana scale fan plays or nearly two Permian Basins.

The largest 30 major oil companies face a 40% production decline of 300-billion-barrels by 2050, according to Wood Mackenzie. Fields currently online will delivery only 700 billion barrels of the almost 1,000 billion barrels needed to meet cumulative liquids demand through 2050. This amount is equivalent to 14 Guyana scale fan plays or nearly two Permian basins. The situation is most acute for national oil companies and the Euro Majors that on average will need to access more than 1 million boe per day or roughly 50% of their current production base to maintain production and meet future demand.

To meet this shortfall global majors are focusing on yet unexplored ultra-deepwater basins which are expected to account for 60% of planned drilling in 2026. Africa is set to lead global activity accounting for around 40% of planned high-impact exploration wells, driven largely around the Atlantic margin. West Africa has become a focus area as geological similarities between Africa’s undeveloped west coast and huge productive basins on the other side of the Atlantic Ocean hold the promise of massive discoveries. South America and Africa are geological twins bounded by a shared geological history with multiple discoveries in West African margin mirroring successes in eastern South America, particularly Brazil. Since 2020, 11% of the oil and gas discovered or some 8.7 billion barrels of oil equivalent (boe) has been found throughout West Africa.

¹ TechnipFMC is a leading global technology provider to the traditional and new energy industries, delivering fully integrated projects, products, and services.

Africa is set to lead global activity accounting for around 40% of planned high-impact exploration wells.

Exhibit 1: High Impact Wells by Region (2026)

Source: Wood Mackenzie, Granite Point Research

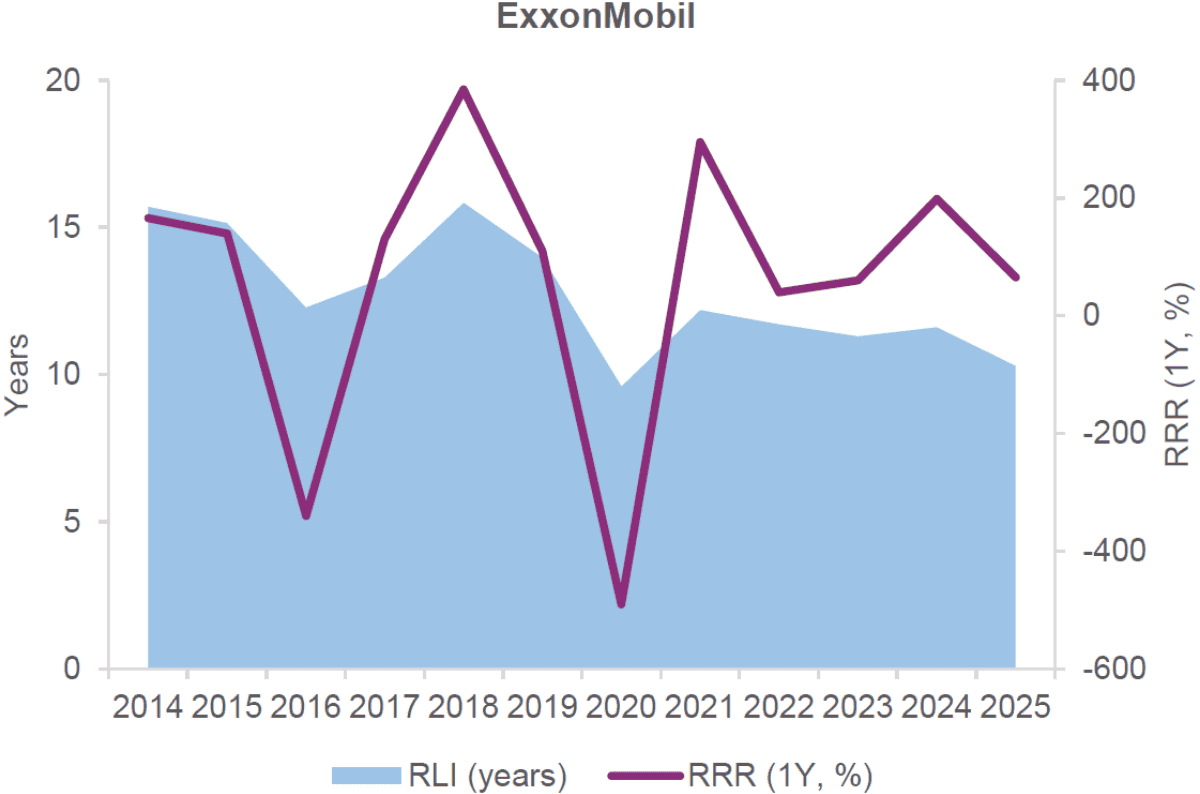

Rapid Depletion of Reserves Driving a Renaissance in Exploration

High impact exploration is enjoying a renaissance driven by the rapidly depleting reserves of the super majors. Exploration is being driven by the need to replace rapidly depleting reserves and to ensure long-term energy security. This renewed focus on exploration is also driven by the looming industry supply gap and a broader pivot away from costly renewable investments.

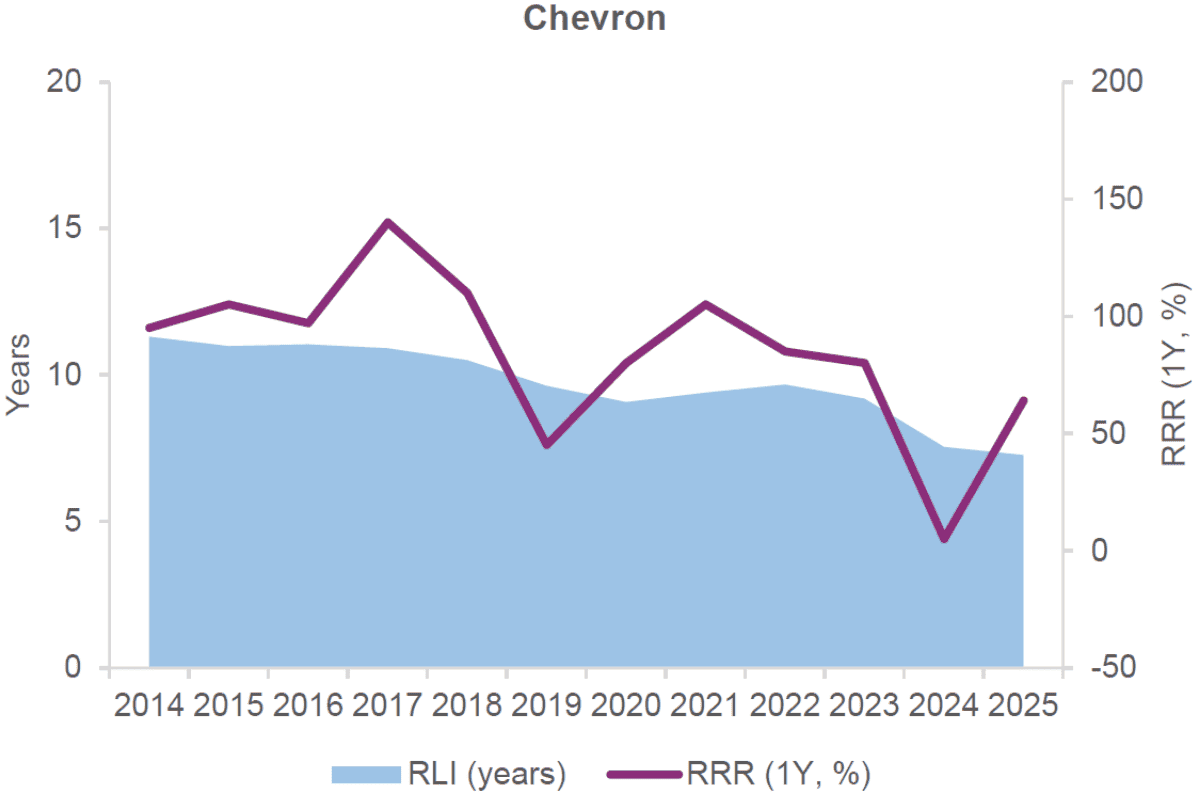

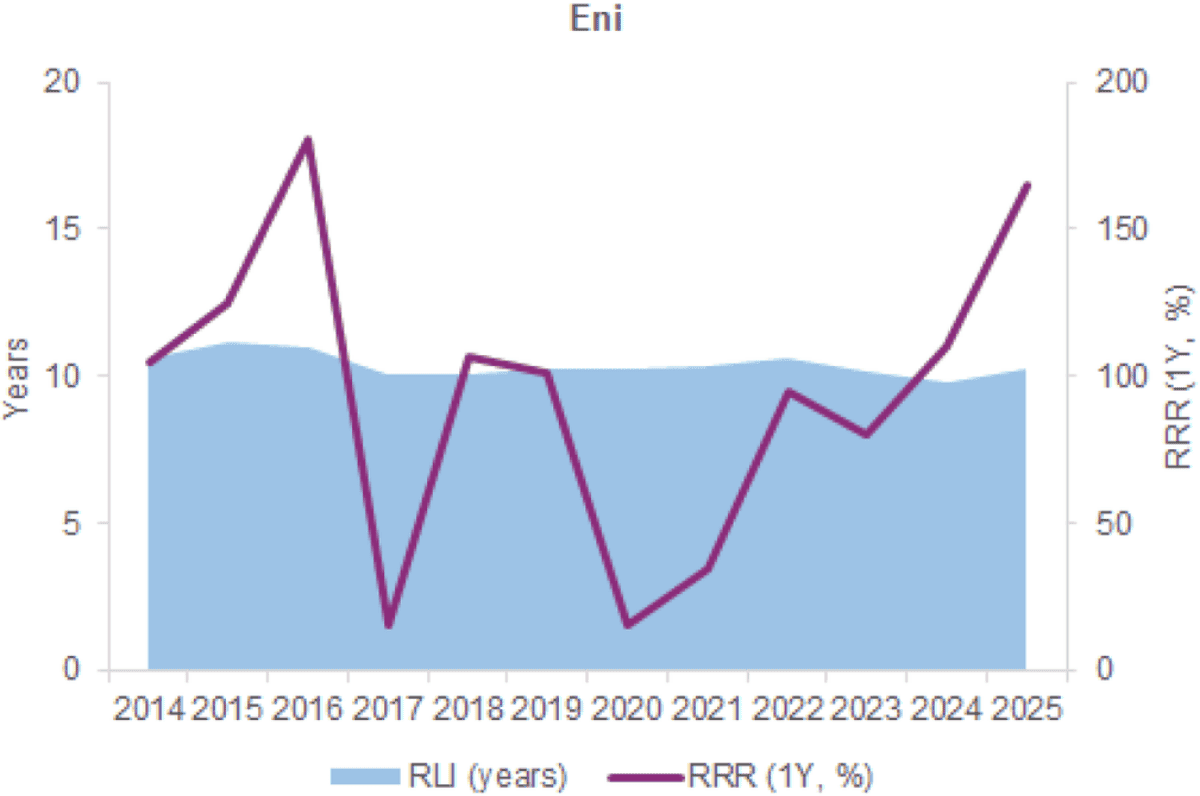

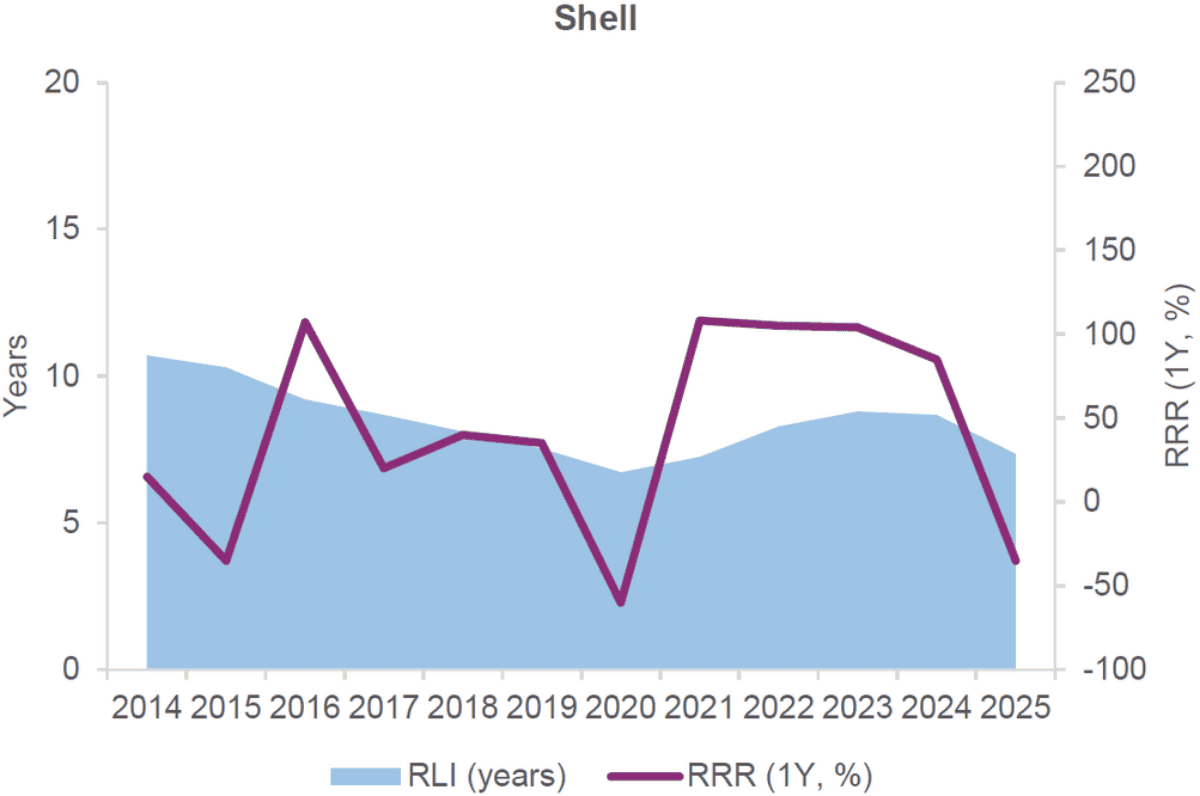

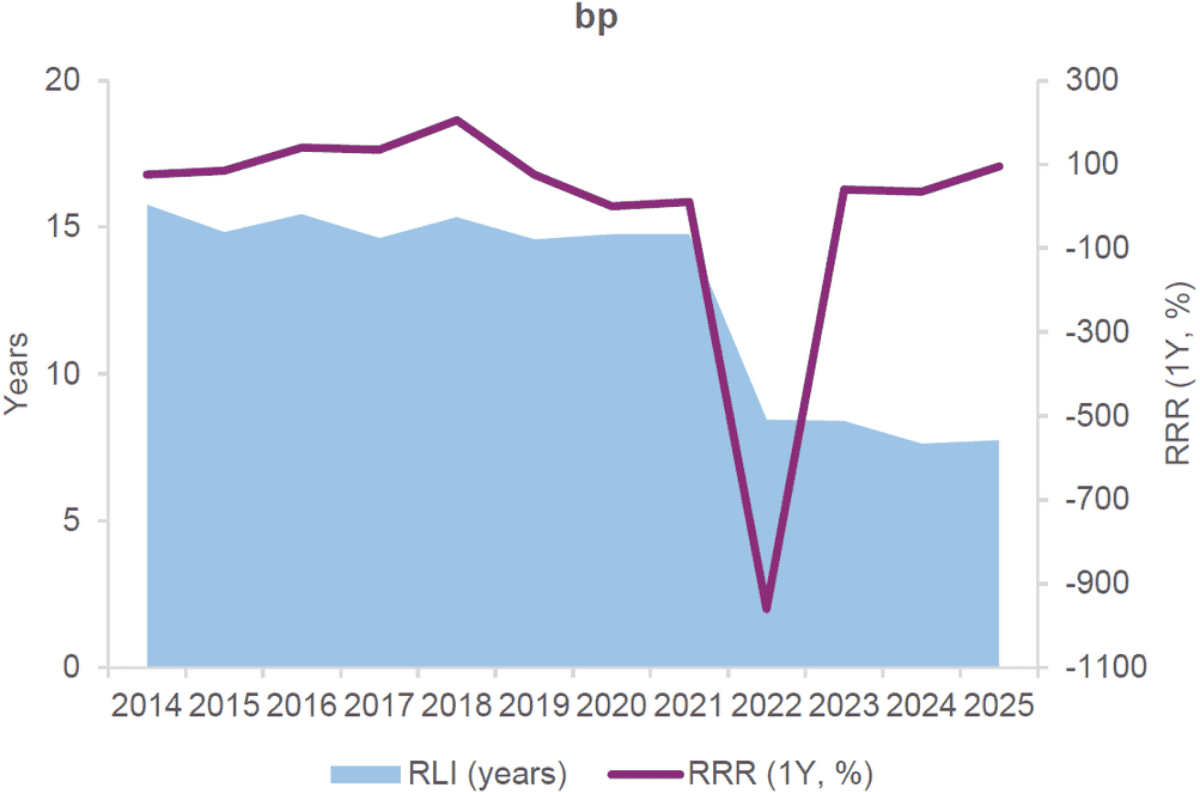

The RLIs for BP, Chevron and Shell has fallen below eight years while the RRRs for six of seven super majors is just 77.3% suggesting a possible decline in future production.

The super majors need to grow their reserves substantially to offset depletion. The reserve life index (RLI) is a key industry metric which measures the number of years of reserves a company has left based on its current rate of production. Without new discoveries, it also measures how many years of production these companies would have left before they exhaust their reserves. For BP, Chevron and Shell, their RLIs have fallen below eight years a situation that must be addressed with a focus on exploration.

Another key metric for the industry is the reserve replacement ratio (RRR) which measures how successfully a company is replenishing its extractable reserves compared to the amount it produces. The average RRR for six of the seven super majors is just 77.3% meaning that the companies are shrinking their reserve bases signaling a possible decline in future production.

Exhibit 2: ExxonMobil RLI and RRR

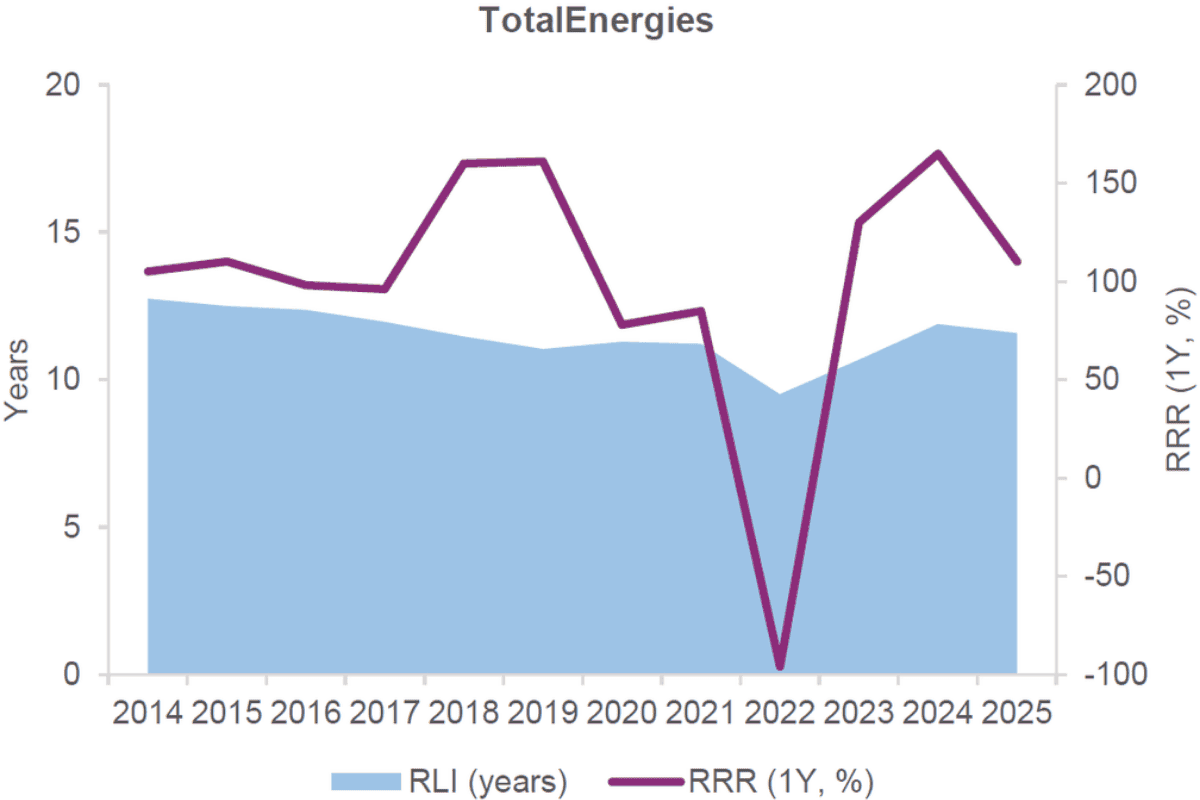

Exhibit 3: TotalEnergies Had a Strong Recovery From 2022

Exhibit 4: Chevron’s RLI Is Below 8 Years

Exhibit 5: Eni RLI Has Had a Strong Post-2022 European Recovery

Exhibit 6: Shell’s RLI Is Below 8 Years

Exhibit 7: BP’s RLI Is Below 8 Years

Source: Enervus, Granite Point ResearchTechnology has allowed energy companies to push into ultra-deepwater basins looking for giant oil and gas fields. Energy companies are drawn to these ultra-deepwater, and frontier plays because they offer scale and material upside at a time when conventional opportunities are increasingly limited. Deepwater drilling has been a strategic focus for big oil companies for several years now, as fields in shallower waters mature and production declines. Ten years ago, the technical cutoff for deepwater wells was ~2,000 meters but today it is ~4,000 meters where ultra-deepwater is defined by drilling water depths of 1,500 meters or more. Some of the technological advances that have unlocked reservoirs in 3,900-4,000 meters depth include:

•Massive eighth-generation drillships with 3.4 million-pound hookload capacity that allow operators to run miles of heavy casing strings.

•Dynamic Positioning (DP) Systems: Satellite-linked GPS and thruster controls allow ultradeepwater drillships to maintain precise positioning over the well negating the need for physical anchoring systems

•Advanced Subsea Processing: Deep subsea pumps and boosting systems are directly installed on the sea floor to assist with fluid transport to surface-based Floating Production, Storage, and Offloading (FPSO) vessels.

•Intelligent Drill Pipes: Pipes with built-in magnetic coupling rings that allow for higher data transmission rates and real-time down hole monitoring.

•Managed Pressure Drilling (MPD): A drilling process used to control the dynamic annular pressure profile. It continuously adjusts the downhole pressure environment to ensure precise wellbore stability, and to prevent kicks or fluid losses.

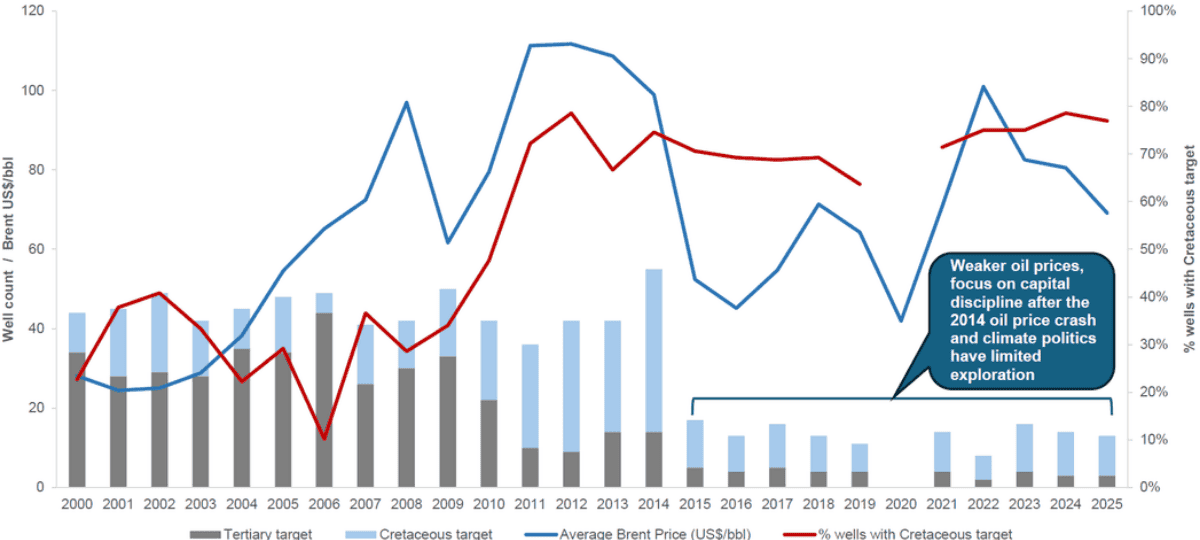

Cretaceous Plays Dominate Wells Drilled in Offshore West Africa

Since 2011 Cretaceous-aged plays dominate wells drilled in offshore West Africa. In the past decade two thirds of West African exploration wildcats were Cretaceous targets. The first wave of deepwater exploration successes in West Africa were centered on large Tertiary deltaic plays such as those in the lower Congo basin and the Niger Delta. In the last decade, the focus has shifted toward Cretaceous plays with breakthrough Cretaceous discoveries on both sides of the Atlantic margin. Cutting-edge seismic acquisition and imagining technologies along with enhanced deepwater drilling capabilities coupled with advances in geological understanding and basin modelling have been the primary drivers of this change. Exhibit 8: Offshore West Africa Exploration Wells Are Overwhelmingly Cretaceous Wells

Source: Wood Mackenzie, Granite Point Research

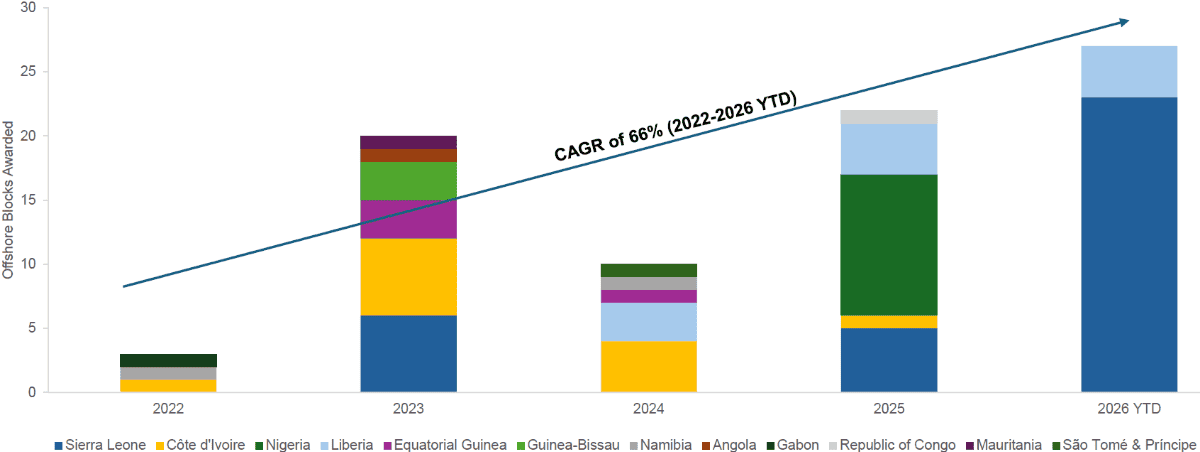

Offshore Block Awards Accelerating Rapidly in West Africa

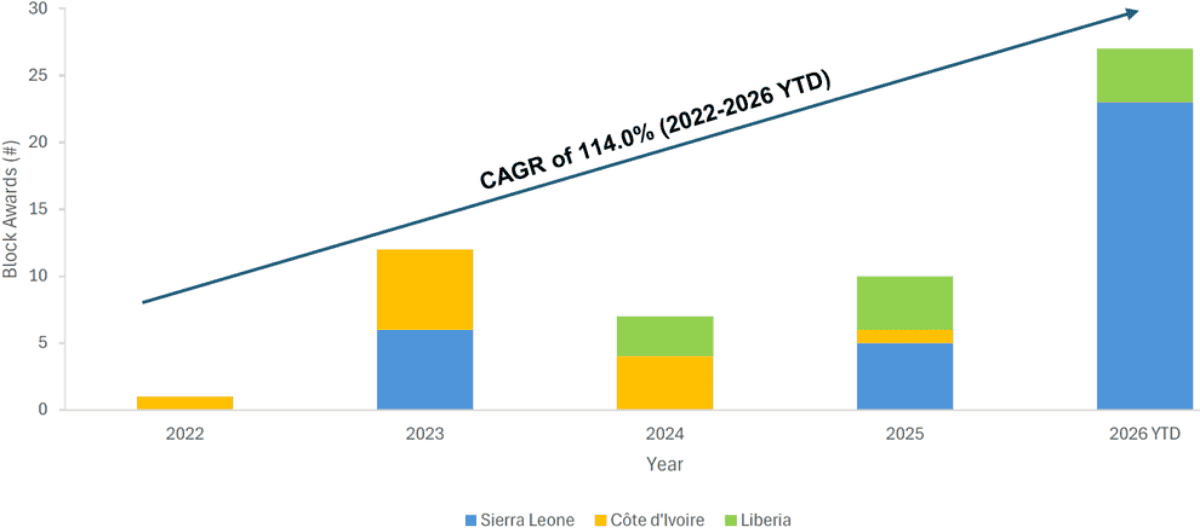

Liberia, Côte d’Ivorie and Sierra Leone account for 69.5% of offshore West African block awards growing at a CAGR of 114% (2022-2026 YTD).

West Africa is the epicenter of global exploration and that trend is accelerating. Between 2022-2026 YTD West African offshore block awards grew at a CAGR of 66%, but most of that growth (69.5%) occurred in just three countries: Liberia, Côte d’Ivorie and Sierra Leone. These three countries have grown block awards at a CAGR of 114% (2022-2026 YTD). Between 2025 and 2026 YTD block awards for these three countries accelerated to 170%, a rate that does not include an anticipated Liberian license round in June 2026.

Between 2025-2026 YTD this rate accelerated to 170%.

A scramble is underway by global super majors and NOCs to secure majority ownership in frontier prospects to secure advantaged resources that can displace higher-cost production and help plug the industry’s 300-billion-barrel supply gap. Ultra-deepwater successes by Eni SPA in Côte d’Ivoire and TotalEnergies (Venus – offshore Namibia) is helping to spur intense interest in offshore West Africa. Offshore West Africa exploration has an excellent track record with the sector creating US$120 billion in value between 2021 and 2025 at US$85 per barrel Brent after deducting US$97 billion of exploration and development spend, according to Wood Mackenzie.

Exhibit 9: Block Awards in West Africa Are Growing at a CAGR of 66% (2022-2026 YTD)

Source: Granite Point Research Exhibit 10: …Liberia, Sierra Leone & Côte d’Ivorie Account for 69.5% of Block Awards which Have Grown at a CAGR of 114% (2022-2026 YTD)

Source: Granite Point Research

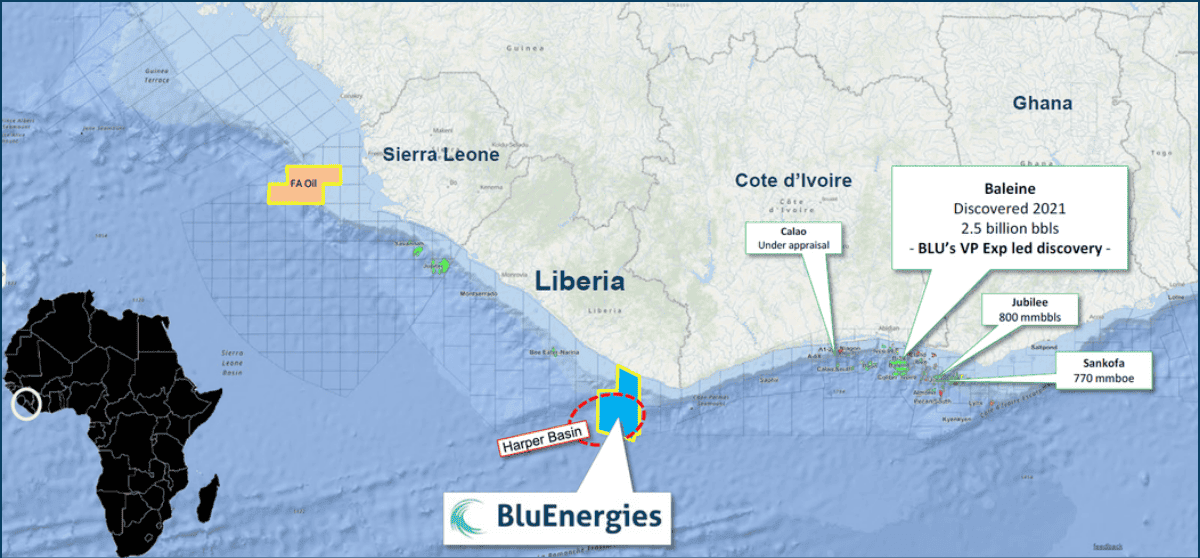

BluEnergies Stands as the Lone Junior in a Land of Giants

BluEnergies (covered by GPR) is the only junior public company with pure play exposure to multi billion-barrel deepwater fan plays.

We initiated coverage (view report) on BluEnergies Ltd.² (BLU – TSXV, BLUGF – OTCQX, F66E) in March 2026 with a Buy rating and a C$4.75 price target. As the only junior public company with pure play exposure to multi-billion-barrel fan plays, we view BluEnergies as being well positioned for dramatic growth. The Company’s partnership (BLU 35%; TTE 65%) with TotalEnergies (NYSE and Euronext: TTE – not covered) represents a tremendous vote of confidence in the Harper Basin and BluEnergies itself. We believe that in the Company’s license area there is a multi-billion-dollar boe prospective resource potential and risk has been reduced with BluEnergies’ partnership with TotalEnergies.

We view BluEnergies as being extremely wellpositioned for dramatic growth.

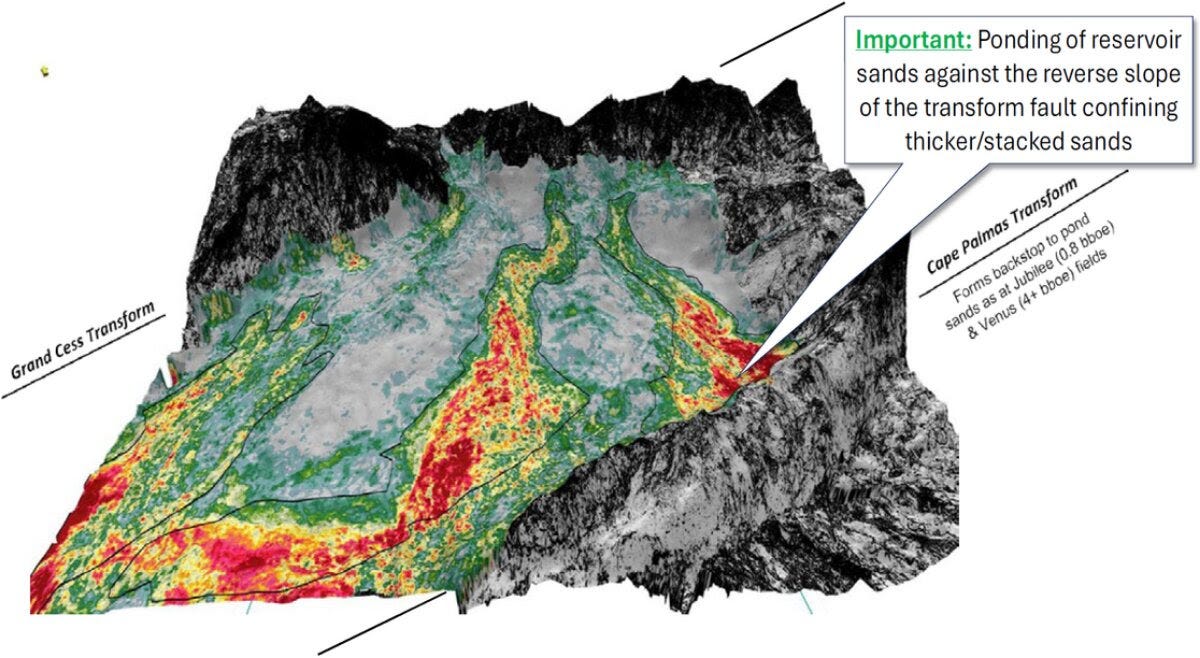

As a first-mover in 2024 BluEnergies was able to choose the best basin — a constrained basin with thicker depositional sands. BluEnergies’ three blocks in the Harper Basin (~40% of the basin) have a thicker reservoir in their fault-bounded basin which is confined to a small area. We believe that there are multiple stacked reservoirs because of a ponding effect occurring in the Harper Basin.

Since 2024 there has been a 550% increase in licensing activity along the West African Transform Margin near BluEnergies’ blocks. In 2024, BluEnergies secured three blocks in the Harper Basin in offshore Liberia the only junior in the region. Since then, they’ve partnered with TotalEnergies and seen Oranto, Eni, Shell, ExxonMobil, Marginal Energy, Chevron and Petrobras become their neighbors.

² See pages 10-11 for important research disclosuresExhibit 11: 2024 - BluEnergies Secures First-Mover Advantage in Offshore Liberia

Source: Company reports Exhibit 12: 2025/2026 – New Entrants Flock to the West African Transform Margin

Source: Company reports

First Mover Advantage Helped BluEnergies Secure the Best Blocks

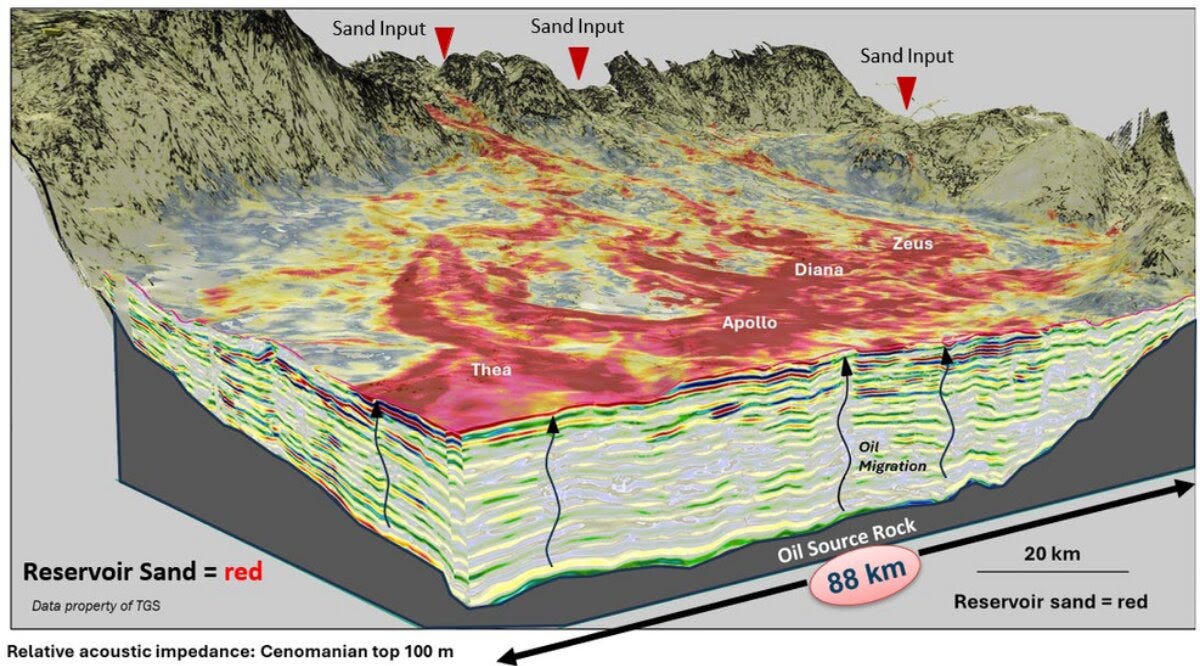

The Harper Basin is likely the last undrilled sedimentary basin in offshore Africa.

The Harper Basin is likely the last undrilled sedimentary basin in offshore Africa. BluEnergies has discovered seven deep water basin floor fan plays on its license area with multibillion-barrel potential. Fan plays typically have stacked sands and multiple targets that can be tested per well with typically high production rates per well. West African Cretaceous-aged wells achieved a greater than 50% technical success rate from 2015-2025 which is significantly above the global average, according to Wood Mackenzie.

The Harper Basin is a relatively narrow basin occupying an area of 20,000 square kilometers that was formed between two major transform fracture zones. The basin extends from shelf to basin floor in an embayment formed between two transform ridges: Cape Palmas/St. Paul Transform Zones to the south and Grand Cess Transform Zone to the north.

Basin floor fan plays typically offer faster payouts and better economics, making them extremely sought after by industry. Deepwater basins often hold a significant portion of the world’s undiscovered oil and gas with recent discoveries such as TotalEnergies’ Venus-1X discovery in Namibia’s Orange Basin (2022) being a case in point. These structures often contain very large fields including giant fields (over 1 billion barrels of oil equivalent), indicating a substantial potential for future production. Also, deepwater wells often have high estimated ultimate recovery figures per well, meaning that fewer are needed to extract the same volume of hydrocarbons when compared with conventional onshore production thereby improving project economics.

Source: Company reports

Risks for BLU Stock Biased to the Upside

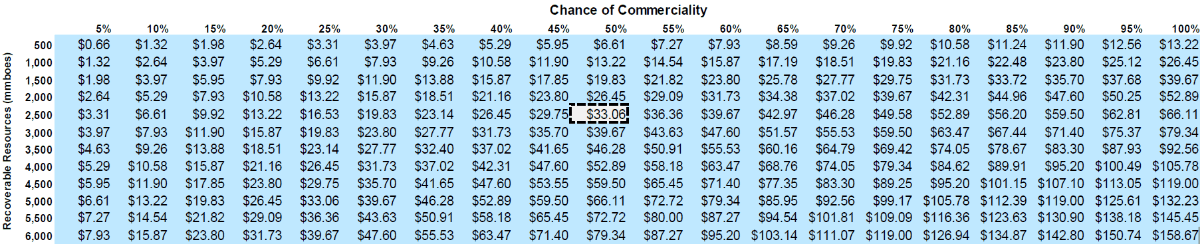

We believe that shares in BluEnergies represent an extremely attractive risk/return proposition with substantial potential upside as the partnership with TotalEnergies develops and these blocks are de-risked.Target price sensitivity to the chance of commercial success (CoC): There is considerable upside beyond our $4.75 per share target price as either the chance of commercial success or the level of recoverable resources improves. Our sensitivity table below shows various levels of prospective resource levels ranging from 500 to 6,000 million boe and varying chances of commercial success. Exhibit 15: There Is Significant Upside Potential for BluEnergies’ Stock (Based on BLU’s 35% Working Interest – Projected NAV/Share)

Source: Granite Point Research

Asymmetric investment opportunity. We believe BLU represents a unique value proposition.

Asymmetric investment opportunity. We believe that the large potential upside in the shares of BLU represents a unique value proposition as the only publicly listed pure play junior in the region with a world class partner (TotalEnergies) which in our view creates an asymmetric investment opportunity. BluEnergies first mover advantage allowed the Company to secure access to three blocks (~40% of the basin) in the Harper Basin on preferential terms that would be unlikely for it to replicate today. The Company has a significant working interest of 35%, which may attract farm-out opportunities which could provide very attractive optionality for the Company and could lead to a strong valuation boost. We reiterate our Buy rating and $4.75 target price.